After years of global uncertainty, volatility in the M&A market has long become the new normal. Inflation, rising interest rates, and geopolitical tensions are shaping the environment – and yet, the market for small and medium-sized enterprises in the DACH region is proving resilient. In the first half of 2025, 21 percent of market participants reported increasing transaction volumes, while 63 percent recorded stable values. It is particularly noteworthy that the share of larger transactions over 10 million euros has increased by eight percent. Smaller deals in the range between 2.5 and 5 million euros, on the other hand, declined significantly. This indicates a shift towards fewer but higher-volume transactions – a clear sign that investors are acting more selectively and strategically.

Industry dynamics reinforce this impression. Software development was cited by 31 percent of consultants as the sector in which the most additional deals are expected for the second half of the year. Healthcare came in second with 16 percent, followed by business services with 15 percent. Declines, on the other hand, are mainly seen in the automotive, transport, and logistics sectors, where 32 percent of those surveyed predict fewer transactions. The retail sector (23 percent) as well as gastronomy, tourism, and leisure (12 percent) also remain under pressure. The industrial core of the Mittelstand thus demonstrates remarkable resilience – while parts of the “Old Economy” are losing market share, future-oriented sectors are gaining significantly in attractiveness.

At the same time, the financing landscape is changing. 44 percent of the consultants surveyed stated that access to capital has become more difficult, with only nine percent reporting an improvement. Lenders are demanding higher equity ratios and stronger collateral, which is raising the hurdles, especially for smaller transactions. Contract clauses are adapting to this reality: earn-outs and seller loans are being used much more frequently. 51 percent of the consultants reported an increase in earn-outs, and 48 percent reported an increase in seller loans – an expression of a growing willingness to distribute risks fairly between the buyer and seller sides.

Valuations also paint a differentiated picture. The average EBITDA multiple remains stable at 5.55. At the upper end are software development with 8.9 and Healthcare & Pharma with 8.4. In the classic industrial segment, the value is 5.3, while the automotive sector comes in at only 4.3 and the retail sector brings up the rear with 2.8. This spread clearly shows how much investors today are looking for structural sustainability and business models with resilient demand.

| Industry | Multiple H1-2025 | Change vs. H2-2024 | Change vs. H2-2024 |

| Industry & Production | 5.3 | ±0 | Stable Mittelstand core, resilient |

| Software development | 8.9 | +0.2 | Highest multiple; most frequently mentioned future sector (31%) |

| Transport & Logistics | 4.3 | -0.1 | 32% expect decline – clear negative trend |

| Healthcare & Pharma | 8.4 | +0.1 | Strong demand, 2nd place in expected deals (16%) |

| Business services | 5.7 | +0.2 | 3rd place in expected deals (15%) |

| Retail | 2.8 | -0.1 | Weakest multiple; 23% expect fewer deals |

| Gastronomy, Tourism & Leisure | 3.1 | -0.2 | 12% expect declines; structurally under pressure |

An additional factor that is changing the market is the use of artificial intelligence. 29 percent of consultants stated that they regularly use AI in M&A processes – in 2023, it was only seven percent. Efficiency gains are thus being achieved, particularly in market research, company valuations, and the identification of off-market opportunities. At the same time, the focus after closing is shifting more and more to operative levers: integration, scaling, technology expansion, and location optimization are increasingly determining the success of a transaction, while short-term valuation fantasies are losing importance.

As a specialized corporate finance consultancy for the industrial Mittelstand, we support entrepreneurs, investors, and corporate groups throughout the entire M&A process – from succession arrangements and carve-outs to targeted search and valuation, through to post-closing integration and operative value realization. Our approach combines structure, substance, and scalability. In this way, M&A in the Mittelstand does not become a risk, but a strategic lever for the next growth and transformation phase.

You can read more details on dealsuite.com.

Related Posts

GovTech in Germany: M&A Report on Public Sector Tech, Municipal Software, and Administrative Software

How the market for IT & software in public administration is being reshaped –…

Securing the Preservation of a Legacy

starkpartners consulting in the magazine "Standort Meerbusch" - We support…

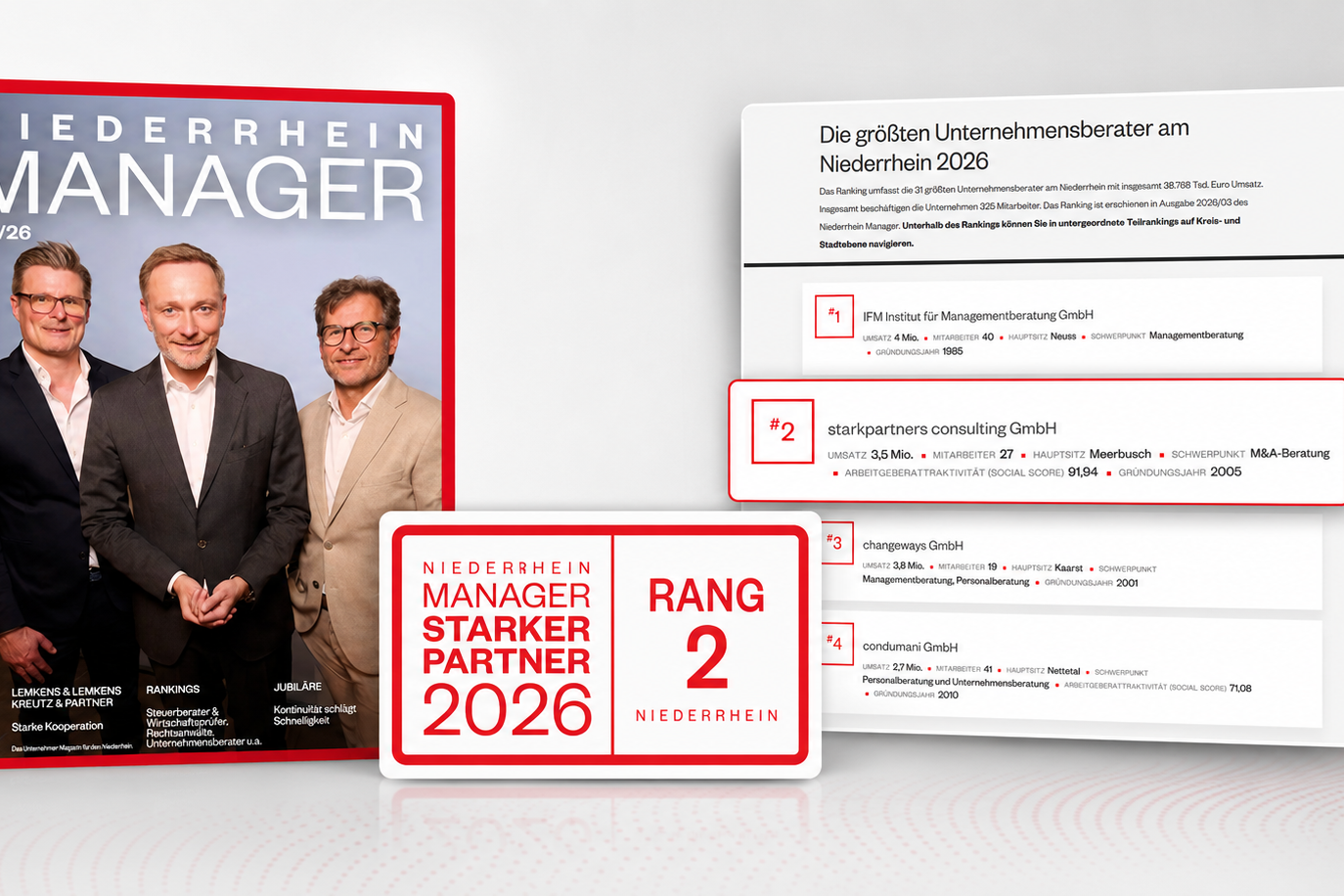

Ranked 2nd in the Lower Rhine ranking of the largest management consultancies

We are delighted that starkpartners consulting has been ranked 2nd in the…