The global software market is one of the most resilient and fastest-growing segments of the global economy. It is characterized by high, long-term stable revenue potential, low dependence on macroeconomic cycles, and significant economies of scale through digital value creation. These structural characteristics make software companies a strategic lever for sustainable, capital-efficient growth—and thus an extraordinarily attractive investment opportunity.

In particular, companies in the Software as a Service (SaaS) sector have achieved above-average growth in recent years and have proven their robustness even in phases of economic uncertainty. While numerous industries recorded significant losses in economically volatile phases, such as during the COVID-19 pandemic, the software industry benefited from the accelerated digitization of almost all sectors of the economy. This structural surge in demand continues to have an effect today.

Transaction activity in the software M&A market reached a historic high in 2021 with a global deal value of around USD 456.9 billion. The subsequent phase of rising interest rates, geopolitical uncertainties, and a revaluation of growth-oriented business models led to a temporary cooling, but did not mark a structural turnaround.

Current industry analyses forecast an aggregated transaction volume of up to around USD 307.7 billion again for 2025. This development is driven in particular by large-volume, often transatlantic transactions. This development underlines that software continues to be one of the most active and strategically relevant M&A segments.

Key value drivers in M&A

A central growth driver of the software market lies in the special nature of the product itself. Once developed, software can be scaled almost indefinitely without proportionally increasing production or material costs. In contrast to capital-intensive industries, growth does not primarily occur through the expansion of physical capacities, but through efficiency gains, innovation, and market penetration. This structure leads to high margin potential and makes software companies particularly attractive to investors.

In addition, there are pronounced network effects and high switching costs. As the user base grows, the value of many software and platform models increases through better data basis, increasing functionality, and higher integration density. Customer processes, data, and workflows are deeply embedded in the respective software, which leads to high customer loyalty and sustainable competitive advantages. Once a provider has reached a critical mass, it becomes increasingly difficult for new market participants to enter the market.

Against this background, key performance indicators for customer loyalty play a central role in the valuation. The Churn Rate is considered an essential indicator for the stability of a business model. Software and SaaS companies have particularly low churn rates compared to other industries – typically around 3%–5% in the enterprise segment and 5%–7% for small and medium business models.

In addition, retention metrics are becoming increasingly important. A Net Revenue Retention of over 110% is regarded by investors as a strong signal for organic growth, product-market fit, and successful upselling strategies. Recurring revenues, measured by Annual Recurring Revenue (ARR), form the central valuation anchor in software transactions. Accordingly, around 61% of the global software M&A volume in 2024 was attributable to SaaS deals.

The software market is gaining additional momentum through the increasing integration of artificial intelligence. AI-based functions open up new fields of application for software companies, increase productivity, and enable clear differentiation from competitors. Accordingly, M&A interest in the AI-related environment is strong. The transactions shown in the field of robotics and automation illustrate the strategic nature of this development: Investors are securing early access to data, technology, and intellectual property.

M&A deals in the software sector (excerpt)

The continuing high M&A interest is also reflected in the market structure. Consolidations, vertical expansions, and targeted market entries characterize the industry. Acquisitions often serve less for classic market development, but for the targeted acquisition of customer bases, technology, and data. Software transactions in particular are not only financially but also regulatorily demanding, as they regularly involve the handling of sensitive customer data and usage profiles.

The software market also remains active at the DACH region level. In recent years, numerous software companies have been acquired, with a clear preference for private equity-driven buy-and-build strategies, particularly in the lower-middle market. At the same time, alternative transaction structures such as minority shareholdings, earn-out models, and joint ventures are gaining in importance in order to limit risks and still participate in high growth opportunities.

This makes it clear that for many investors, the software market is by no means just a normal acquisition area — it has become a strategic playing field for acquiring technological assets, customer loyalty, and data-driven competitive advantages from a single source.

No other market segment combines the advantages of global scalability, strong network effects, recurring revenues, digital distribution channels, and M&A-driven consolidation as consistently as the software market. This interaction leads on the one hand to a market-wide “hockey stick” effect, in which growth and value creation increase exponentially, and on the other hand to multiples that historically reach extraordinary dimensions compared to other industries.

Significance for medium-sized businesses

This revaluation led in the short term to a decline in transaction activity and to a clear shift in investor focus: away from pure growth and towards profitability, cash flow stability, and efficiency.

Today, a much more sustainable market environment is emerging. High-quality software companies with a clear positioning, high customer loyalty, and solid earnings are again achieving attractive valuations. This creates strategic opportunities, especially for German SMEs: Specialized software solutions, flexible organizational structures, and established customer relationships make medium-sized providers sought-after targets – especially within the framework of buy-and-build strategies.

For German SMEs, this means that those who actively seize opportunities now – be it through organic growth, partnerships, or targeted acquisitions – can strengthen their market position, realize economies of scale, and hold their own against larger competitors in the long term. In a market environment in which large-volume mid-cap transactions are currently losing momentum, companies have a strategic opportunity to specifically strengthen their own competitive position and use M&A as an effective lever for sustainable growth.

In addition, there are also additional potentials for German SMEs at the geographical level. Current market forecasts indicate that Europe will be one of the most attractive regions for tech M&A in the coming twelve months. The German software SME sector can thus benefit from a regional market phase that particularly favors investments, consolidation processes, and strategic partnerships.

How does starkpartners support in this market environment?

In the dynamic environment of the software industry, a deep understanding of software-typical valuation logics, transaction structures, and market mechanisms is crucial. Many software companies face the challenge of securing growth capital, selectively expanding their customer base, and expanding technological and entrepreneurial expertise through strategic acquisitions or cooperations.

Currently, starkpartners is responsible for the investor processes of two software companies, combining comprehensive transaction experience with pronounced industry expertise.

Our approach is entrepreneurial: We identify investors and partners who not only provide capital, but also understand the special value drivers, dynamics, and sensitivities of the software market.

On this basis, transactions are structured that secure innovations, preserve entrepreneurial substance, and enable long-term growth.

starkpartners stands for discreet, entrepreneurial advice at eye level with a pronounced technological understanding, high sensitivity for company data, and deep respect for the life’s work of our clients.

Related Posts

GovTech in Germany: M&A Report on Public Sector Tech, Municipal Software, and Administrative Software

How the market for IT & software in public administration is being reshaped –…

Securing the Preservation of a Legacy

starkpartners consulting in the magazine "Standort Meerbusch" - We support…

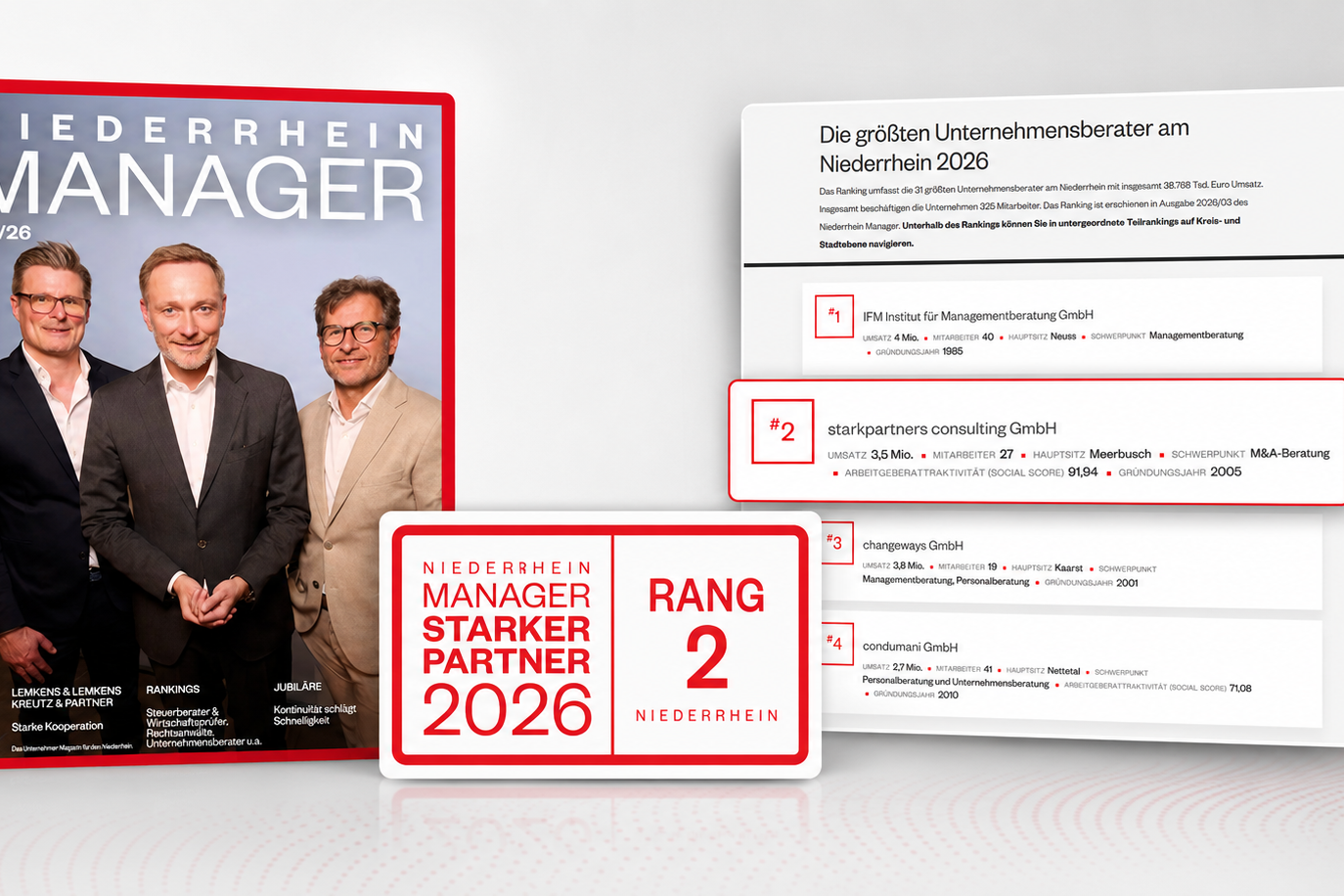

Ranked 2nd in the Lower Rhine ranking of the largest management consultancies

We are delighted that starkpartners consulting has been ranked 2nd in the…