Public Sector Tech: How the GovTech Market in Germany is Consolidating

The GovTech market in Germany—comprising software and IT solutions for municipalities, authorities, and public administration—is evolving from a fragmented niche market into a strategically relevant field of consolidation. The decisive factor is no longer who offers the most functions, but who delivers systems that run reliably in everyday administrative operations, fit into existing structures, and are sustainable in the long term.

The focus is on municipal specialist procedures, administrative software, citizen portals, DMS and e-file solutions, as well as integration and platform approaches that connect various public administration systems. This M&A report contextualizes market dynamics, regulatory drivers, market structure, and valuation logic. The Executive Summary summarizes the core theses; the full analysis, including the market structure matrix, current deal overview, valuation ranges by asset type, and strategic value levers, is available upon request.

Receive the complete M&A report on Public Sector Tech in Germany, featuring in-depth analysis of market structure, deal activity, consolidation clusters, valuation logic, and strategic implications.

Request the full M&A report now.

What is GovTech in Germany?

GovTech encompasses software and technology solutions for the public sector, particularly for municipalities, authorities, and public institutions. These include, among others:

- municipal specialist procedures, e.g., for construction, finance, and social affairs

- administrative software for cities, districts, and municipalities

- citizen portals and OZG (Online Access Act) services

- DMS and e-file systems

- integration and interface solutions, for example in the context of register modernization and NOOTS

- solutions for digital identity and secure cloud infrastructures

The German GovTech market is characterized by a large number of medium-sized providers with high specialization and deep roots in administrative processes. It is precisely this anchoring that makes good providers difficult to replace: process knowledge, references, and integration into daily work routines can hardly be built up in the short term, and switching costs are high. Once a provider is in the system and delivers reliably, they usually stay for the long term.

Why Public Sector Tech is Becoming Strategically Relevant Now

Administration increasingly functions via software, and these very systems are currently being reorganized. Several developments are bringing public sector tech into the focus of investors and strategic buyers:

- increasing pressure to digitalize in municipalities and authorities

- growing importance of interoperability and standardization

- requirements for digital sovereignty and secure IT infrastructures

- shortage of skilled labor in public administration

- shift from individual solutions to integrated system landscapes

The pace is set by new infrastructure at the federal level: the administrative cloud, official data exchange within the framework of register modernization (NOOTS), a digital procurement marketplace, and initial AI pilots in municipalities. In parallel, a stricter BSI Act has been in force since December 2025. Many solutions already exist but do not function reliably in everyday life, and a significant portion of digitally available services is not yet in widespread use. This does not make the market more arbitrary, but more demanding, which increases the value of resilient specialists.

Overview of Municipal Software, Specialist Procedures, and Platforms

The market for software in public administration can be divided into several segments that are increasingly merging and forming the basis for integrated GovTech platforms:

- Municipal specialist procedures – specialized software for specific administrative processes

- Administrative software, DMS, and e-files – document management, case processing, and workflow

- Citizen portals and frontends – digital interfaces for citizens and businesses

- Integration and platform solutions – connection and orchestration of different systems

- Administration-related specialist software – solutions for adjacent areas such as education, health, or infrastructure

How the Market is Structured

The market is fragmented but strategically easy to read. Two axes organize it: proximity to the public sector (deeply anchored to adjacent) and solution breadth (specialized to platform). This results in four provider groups:

- public sector specialists for specialist procedures and administrative processes

- broad public sector platforms with deep anchoring in administration

- enablers for integration, operation, and transformation

- vertical specialists in adjacent, publicly influenced sectors

Providers that are difficult to replace or easy to expand are particularly attractive. Established platforms are also under pressure to translate their historically regional strength into nationwide connectivity and partnership capability.

In the full report: the market structure matrix with classification of relevant providers and strategic white spots.

M&A Trends in the German GovTech Market

M&A activity in public sector tech follows recognizable patterns: consolidation of municipal specialist procedures, development of integrated platforms and software stacks, investments in specialized niche providers, and increasing interest from private equity investors, supplemented by initial movements around AI, security, and digital sovereignty. Visible transactions point less to a broad buyout wave and more to the targeted reorganization of individual asset types: bundling specialist procedures, forming platforms, and integrating enablers. Movement occurs primarily where software is deeply embedded in critical administrative processes and is difficult to replace in everyday life.

Demand comes from three directions: strategic software providers expanding their offering; financial investors and platforms looking for scalable business models with recurring revenue; and IT and service-related providers moving closer to the customer through operational and integration expertise.

In the full report: the current deal overview since 2024, consolidation clusters, deal motives, and detailed buyer and platform logics.

Valuation Logic for GovTech and Administrative Software

The valuation of software companies in the public sector follows criteria that differ from classic SaaS logic. The decisive factor is not just growth, but how essential the solution is in the customer’s daily routine. Particularly relevant are deep integration into administrative processes, long-term customer relationships, operational security, integration capability into existing IT landscapes, and connectivity to platform and ecosystem structures.

Broadly, three archetypes can be distinguished: project- and service-related providers, deeply integrated specialists, and platform/complete solutions. Companies with high process proximity and an installed base are typically valued significantly higher than project-driven providers. Depending on the archetype, indicative multiples move in a wide range from high single digits to the lower twenty EV/EBITDA range.

In the full report: indicative valuation ranges per archetype and strategic value levers.

The Role of OZG, Register Modernization, and Digital Sovereignty

Regulatory and political initiatives significantly shape the market and directly impact product requirements, market structure, and M&A activity:

- the Online Access Act (OZG) and its further development

- register modernization and data exchange via NOOTS

- requirements for digital sovereignty and European cloud solutions

- increasing requirements for IT security, for example through NIS2 and the new BSI Act

NOOTS turns standardized interfaces from an advantage into a requirement, the administrative cloud shifts requirements toward sovereignly operable, interchangeable stacks, and security-by-design is becoming a mandatory discipline.

What the Full Report Shows

The report shows how the market for public sector tech in Germany is changing structurally and which providers and asset types will become particularly relevant in the coming years. Insights from the report:

- the central market thesis on the development of GovTech in Germany

- consolidation patterns in the field of municipal software

- the classification of specialist procedures, platforms, and enablers

- strategic implications for investors and market participants

The complete analysis with market structure, deal overview, and valuation logic is included in the full report.

Frequently Asked Questions about GovTech and M&A in the Public Sector

What is meant by GovTech?

GovTech refers to software and technology solutions for the public sector, particularly for municipalities, authorities, and state institutions. These include municipal specialist procedures, administrative software, DMS and e-file systems, citizen portals, and integration and platform solutions.

What software is used in public administration?

Typical examples are municipal specialist procedures for construction, finance, and social affairs, administrative software for cities and districts, DMS and e-file systems for case processing, citizen portals and OZG frontends, and integration and interface solutions in the context of register modernization.

Why is the GovTech market in Germany consolidating right now?

New infrastructure at the federal level is setting the pace: administrative cloud, official data exchange via NOOTS, a digital procurement marketplace, and initial AI pilots, plus the stricter BSI Act since December 2025. While many services are available digitally, they are not yet in widespread use. Administrations need resilient overall systems instead of individual solutions, and providers are bundling specialist procedures and platforms to meet this demand.

How are GovTech and administrative software companies valued?

The role of the solution in the target architecture is decisive, not growth alone. The more difficult an asset is to replace, the more deeply integrated it is, and the more sovereignly it can be operated, the higher the valuation usually is. Depending on the archetype, indicative multiples range roughly from high single digits to the lower twenty EV/EBITDA range; the exact allocation per archetype is contained in the full report.

Which public sector software companies are attractive M&A targets?

Specialists that are difficult to replace with deep expertise in specialist procedures and a high installed base are in high demand, as are expandable platforms with connectivity to nationwide standards. Relevant segments include core administration and specialist procedures, DMS and e-files, OZG frontends with backend connectivity, integration and interfaces, as well as managed services and security.

Which M&A trends are shaping the German GovTech market?

The pattern is the targeted reorganization of individual asset types: bundling specialist procedures, forming platforms, integrating enablers, rather than a broad buyout wave. Movement occurs primarily where software is deeply embedded in critical administrative processes. A complete overview of transactions since 2024 with consolidation clusters and deal motives is included in the full report.

What makes a public sector software provider difficult to replace?

Process knowledge, references, and product logic that intervenes deeply in everyday work routines can hardly be built up in the short term. Switching costs are high, and those once anchored in critical administrative processes usually remain in the system for the long term. Functional expertise and connectivity carry more weight than pure technology.

Why is public sector tech interesting for investors?

Due to stable, long-term customer relationships, high barriers to switching, and a structurally increasing need for digitalization, the market is considered attractive for strategic buyers and financial investors. The market is also becoming more demanding, which increases the value of resilient specialists.

Would you prefer a direct exchange? Daniel Fechner will be happy to personally support you with a confidential discussion for further classification.

T: +49 (0) 2150 7058 210

Related Posts

July 1, 2026

Securing the Preservation of a Legacy

starkpartners consulting in the magazine "Standort Meerbusch" - We support…

June 17, 2026

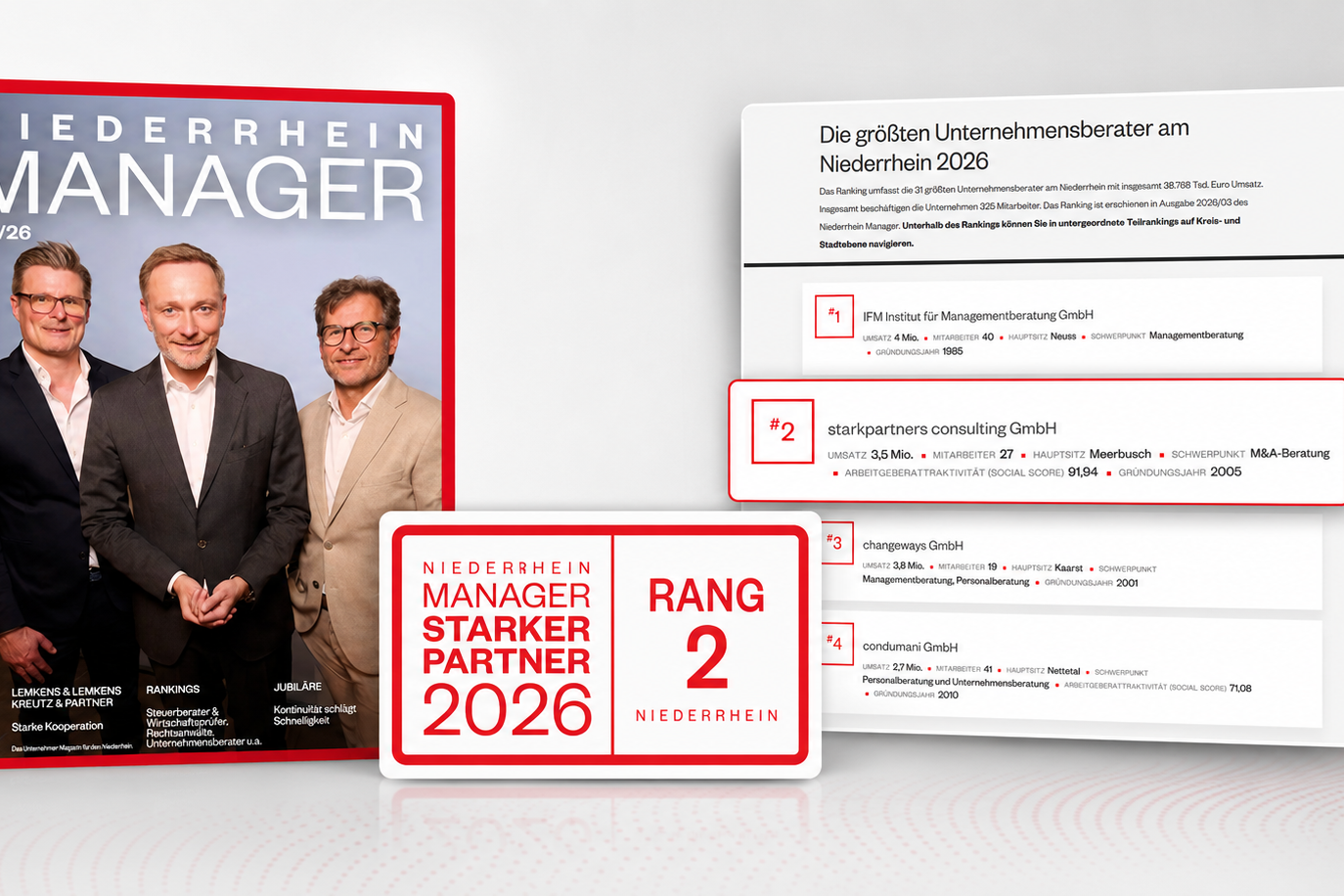

Ranked 2nd in the Lower Rhine ranking of the largest management consultancies

We are delighted that starkpartners consulting has been ranked 2nd in the…

May 27, 2026

Scandinavian Print Group acquires the Limberg Group

starkpartners was responsible for the international distressed M&A process…